Payday and real life almost never line up. Rent, gas, groceries and the odd surprise bill have a habit of landing days before your paycheck does, and the traditional answer — a bank overdraft or a payday loan — is expensive enough to make a tight week worse. FloatMe is one of the best-known apps built to fill that gap. It is a subscription-based cash advance app that lends small, interest-free amounts it calls “Floats” — up to $100 for eligible members — with no credit check, then quietly pulls the money back on your next payday. Alongside the advance it bundles budgeting tools, low-balance alerts, spending insights and a deals marketplace, all for a flat $4.99 a month. With more than seven million downloads and app-store ratings hovering around 4.7, it is a genuinely popular product. But FloatMe also carries an unusual amount of baggage for its size, including a 2024 Federal Trade Commission settlement, and an honest look reveals a real gap between its polished app-store reputation and the experience of some of its members.

For people living paycheck to paycheck who want a small, predictable bridge — enough for gas or diapers, not a $500 loan — FloatMe’s pitch is appealing: no interest, no credit impact, and money in your account fast. Yet the trade-offs are significant. The advance limits are the lowest in the category, you pay a monthly fee whether or not you are approved, and the company’s history with regulators and independent reviewers demands scrutiny before you connect your bank account. This 2026 review walks through FloatMe’s full picture — how Floats and the membership actually work, the new FloatMe Premium tier, real pricing and fees, head-to-head comparisons against EarnIn, Dave and Brigit, the genuine pros and cons, the FTC story in plain terms, and exactly who should (and shouldn’t) sign up.

FloatMe Review 2026: Small Cash Advances, Real Trade-offs, and Life After the FTC

Overview and Background

FloatMe is a San Antonio-based fintech (FloatMe Corp.) that has been operating since around 2018, offering short-term cash advances through a mobile app. It is not a bank and not a payday lender in the traditional sense — it is a subscription service. You pay a monthly membership, connect your checking account, and in exchange you get access to small interest-free advances plus a set of money-management tools. The core promise is simple: when a small expense hits before your paycheck does, FloatMe fronts you a modest amount and takes it back automatically when you get paid, without interest, late fees, or a hit to your credit score.

The company markets itself as your “Best Financial Friend,” and it has scaled quickly — more than seven million downloads, an Inc. 5000 listing, and app-store ratings that sit near the top of the category. It is a licensed and regulated operator: FloatMe Corp. holds NMLS ID #2596392, is registered with the California DFPI under the Consumer Financial Protection Law, and is licensed in Texas as a Regulated Lender Company, with registrations in other states where required. Money moves through Plaid, the same bank-connection layer used by most major fintech apps, and FloatMe states that it uses bank-level encryption, does not store your bank password, and does not sell user data.

There is one part of FloatMe’s history that any honest review has to address up front. In January 2024, the Federal Trade Commission reached a $3 million settlement with FloatMe and its two co-founders over deceptive and discriminatory practices. The FTC alleged that FloatMe lured members with promises of “free” advances of up to $50 while most new users were actually approved for far less (often around $20), charged fees to get money quickly, used “dark patterns” that made cancellation difficult, and unlawfully declined applicants whose income came from public assistance such as Social Security and veterans’ benefits. FloatMe settled without admitting wrongdoing, and the FTC later distributed more than $2.6 million in refunds to roughly 449,000 affected members. Since then, the company has visibly overhauled its disclosures, pricing and cancellation process — which is exactly why the 2026 version of FloatMe deserves to be judged on its current, more transparent form as well as its record.

Why FloatMe Stands Out in 2026

Interest-free by design, with no credit check: FloatMe’s central appeal is that a Float is not a loan in the payday sense. There is no interest, no rolling balance, and no late fee — you borrow a small amount and repay exactly that amount on your next payday. Because there is no credit check to sign up and no reporting of Float activity to Experian, Equifax or TransUnion, a Float can’t hurt (or directly help) your credit score. For someone with thin or damaged credit who just needs to cover gas until Friday, that combination is rare and valuable.

Automatic repayment you don’t have to track: Once you take a Float, FloatMe uses your linked bank connection to withdraw the repayment on your scheduled payday. There is nothing to remember, no manual payment, and no schedule to manage. For people who find due dates stressful, the “set it and forget it” repayment is a real convenience — with the important caveat that you need the funds in your account on that day (more on that below).

The lowest monthly fee among subscription apps: At $4.99 a month, FloatMe’s base membership undercuts most subscription-based rivals. Brigit runs roughly $8.99 to $14.99 a month, and Tilt (formerly Empower) is around $8. Independent roundups repeatedly describe FloatMe as the cheapest pure-subscription option for small advances. If your needs are genuinely tiny and you value the bundled budgeting tools, the low price point is a legitimate advantage.

Budgeting and forecasting built into the same app: FloatMe is more than an advance button. It includes a cash-flow calendar and a financial forecasting feature that estimates your upcoming balance based on past income and spending, plus spending insights and low-balance alerts designed to help you sidestep overdraft fees. Bundling the advance with tools that help you predict when you’ll actually need it is a smarter model than a bare cash-advance app, and it is a genuine part of the value.

A new Premium tier that can build credit: The biggest 2026 addition is FloatMe Premium ($12.99/month), which reports your on-time rent payments to TransUnion — turning an expense you already pay into credit-building history — and adds a Subscription Manager that surfaces recurring charges so you can cancel forgotten trials. Rent reporting is a feature most cash-advance apps don’t offer at all, and it meaningfully changes what FloatMe can do for the right user.

Fast money when you need it: Standard transfers are free and typically arrive within one to three business days, but if you’re in a genuine pinch, an Instant Float can land in your account in as little as a few hours (sometimes minutes) for a fee of $1 to $7 depending on the amount and speed. Having both a free-but-slower and a paid-but-instant option gives you flexibility that a single fixed delivery method wouldn’t.

A visibly reformed, more transparent operator: Post-settlement, FloatMe now spells out its fees in plain language, states clearly that “uninstalling does not result in cancellation,” and lets you cancel in-app at any time. The membership price, the $1 to $7 instant-fee range, and the $10 to $100 Float band are all disclosed on the site. It is fair to be cautious given the history — but it is also fair to note that the current product is markedly more upfront than the version the FTC challenged.

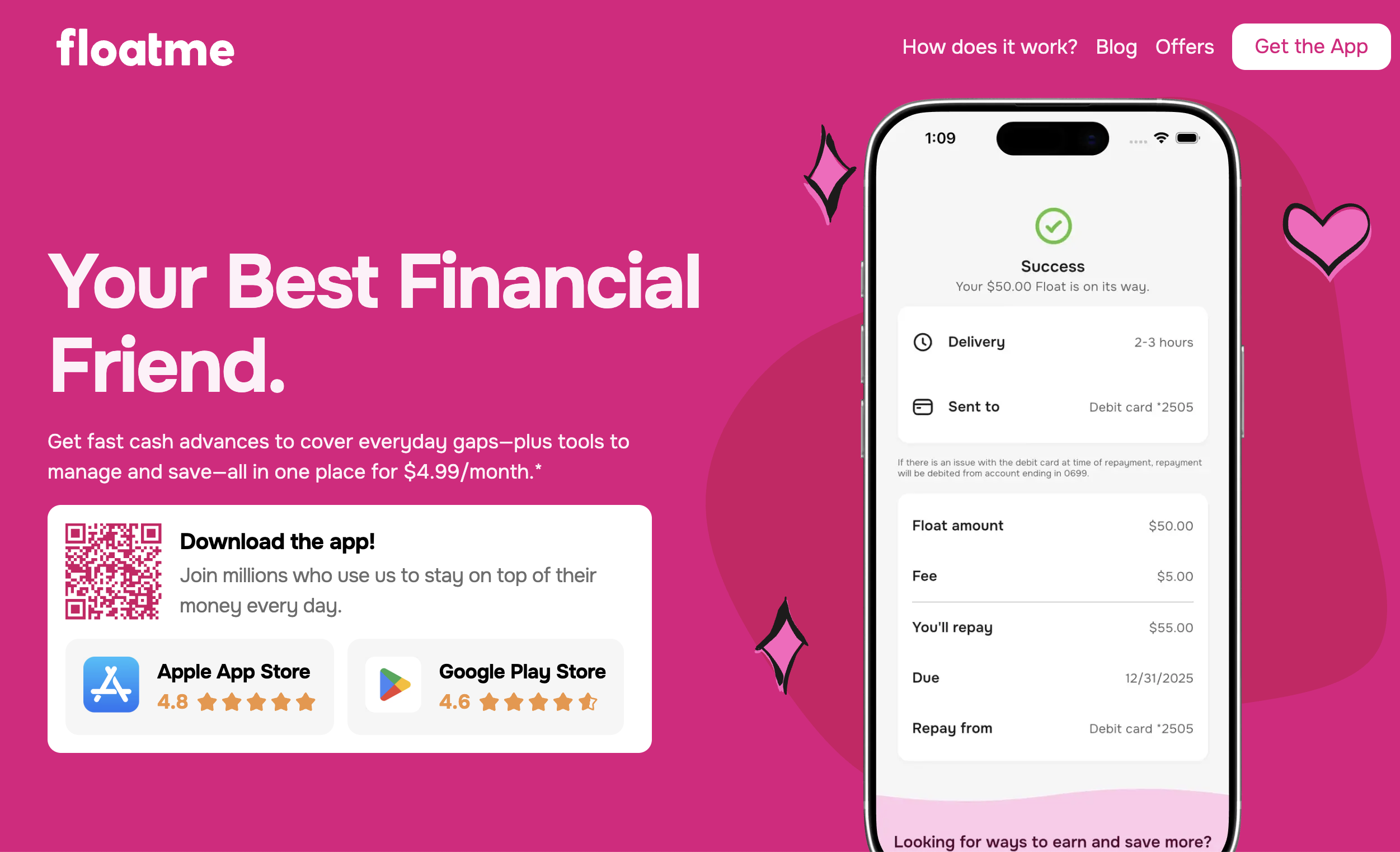

FloatMe fronts small, interest-free “Floats” of up to $100, then automatically pulls the money back on your next payday — a tiny bridge for gas, groceries or an unexpected bill.

Key Features and Technology

FloatMe is a compact app, but its features organize cleanly into a handful of pillars. Here’s how the platform actually breaks down.

Floats: The Core Cash Advance

A Float is a small cash advance ranging from $10 to $100. New eligible members can typically request up to $50 between paydays, with first-time approval amounts landing anywhere from $10 to $50; existing members in good standing can work their way up to $100 over time through consistent, on-time repayment. FloatMe determines eligibility by reviewing the income and spending patterns in your linked bank account — there is no credit check. The honest reality, echoed across independent reviews, is that many members start (and sometimes stay) at the low end, around $20, even with a clean repayment history, so the $100 ceiling is best treated as a long-term possibility rather than a starting point.

Instant vs. Standard Transfers

When you request a Float, you choose how fast you want it. Standard delivery is free and generally takes one to three business days — fine if you plan ahead. Instant delivery costs a fee of $1 to $7, scaled to the size of your Float and the speed you select, and can arrive in as little as a few hours. Importantly, the instant fee is separate from and on top of the monthly membership. This is precisely the fee structure the FTC flagged in 2024 (when the instant charge was a flat $4), so it is worth understanding clearly: the “free” advance is the slow one, and getting money quickly always costs extra.

Budgeting, Forecasting and Alerts

Beyond advances, FloatMe includes a genuinely useful set of money-management tools that come with every membership. The financial forecasting feature projects your upcoming account balance based on your income and spending history, helping you see a shortfall before it happens. Spending insights categorize where your money goes, and low-balance alerts warn you when your balance is running low so you can act before your bank charges an overdraft fee. For members who use these tools rather than only tapping the advance button, they are a real reason the $4.99 fee can pay for itself.

FloatMe Premium: Rent Reporting and Subscription Manager

FloatMe Premium ($12.99/month) keeps everything in the base plan and adds two headline features. Rent Reporting sends your on-time rent payments to TransUnion, so consistent rent history can positively affect your credit score over time — you provide your lease and landlord details once, and the app handles the monthly reporting. The Subscription Manager, powered by Plaid, surfaces every recurring charge in a single dashboard so you can spot and cancel forgotten trials or unused services. Activation takes a few minutes and requires your Social Security number and date of birth to enable credit building; billing is prorated on upgrade, and you can downgrade or cancel in-app at least 24 hours before your next billing date.

Security, Plaid and the Marketplace

FloatMe connects to your bank through Plaid, meaning it never sees or stores your online banking password, and it states that it uses bank-level encryption and does not sell user data. The app also runs a Marketplace of deals on everyday essentials — gas, groceries and bills — where FloatMe earns a commission when members claim offers. That commission, together with membership and instant-transfer fees, is how the company makes money (it earns no interest on Floats). The deals are a small perk rather than a core reason to subscribe, but they’re a low-friction way to offset the membership if the offers match your spending.

Pricing, Plans, and Package Structure

FloatMe runs on a straightforward subscription model with two tiers, plus a per-use instant-transfer fee. Membership is required to request advances, it auto-renews until you cancel, and — this is the part that trips people up — uninstalling the app does not cancel your membership. You must cancel in-app (or via FloatMe’s online form) and wait for the confirmation email. The prices below are FloatMe’s standard rates; the company has changed its pricing more than once (it started at $1.99, later moved to $3.99, and is now $4.99), so always confirm the live price in the app before you subscribe.

| Plan / Item | Price (USD) | What It Is | Best For |

|---|---|---|---|

| FloatMe Base | $4.99 / month | Floats up to $100, budgeting tools, insights, low-balance alerts | Small emergency bridges & everyday budgeting |

| FloatMe Premium | $12.99 / month | Everything in Base plus rent reporting to TransUnion & Subscription Manager | Renters who want to build credit |

| Instant Float Fee | $1–$7 per advance | Optional faster delivery (minutes to hours vs. 1–3 days) | Genuine same-day emergencies |

| Standard Transfer | Free | Included Float delivery, 1–3 business days | Anyone who can plan a few days ahead |

| Interest & Late Fees | $0 | No interest, no late fees, no setup or annual fees | Avoiding payday-loan-style costs |

How FloatMe Compares to Alternatives

| Factor | FloatMe | EarnIn | Dave / Brigit |

|---|---|---|---|

| Max advance | Up to $100 (often ~$20 to start) | Up to ~$750–$1,000 / pay period | Up to $500 each |

| Monthly fee | $4.99 (required) | None (optional tips) | Dave ~$1–$5; Brigit ~$8.99–$14.99 |

| Instant fee | $1–$7 | ~$3.99 (Lightning Speed) | Dave 1.5% (external); Brigit in sub |

| Credit check | No | No | No |

| Builds credit | Only via Premium rent reporting | No | Brigit yes (credit builder); Dave no |

| Eligibility | Bank-activity based; flexible | Strict W-2 / hours verification | Recurring direct deposits required |

| Trustpilot | ~2.2 / 5 (low) | Mixed / moderate | Brigit ~4.5 / 5 (Excellent) |

| Best for | Tiny bridges + cheap budgeting bundle | W-2 workers wanting bigger, fee-free access | Higher limits, credit building, ecosystems |

vs. EarnIn: EarnIn is the sharpest contrast. It charges no mandatory subscription and no required per-advance fee (tips are optional), and it lets qualifying users access up to roughly $750 to $1,000 per pay period against wages they’ve already earned — far above FloatMe’s $100 ceiling. The catch is eligibility: EarnIn is built for W-2 employees with consistent direct deposits and verifiable hours, so gig workers and freelancers often can’t qualify. If you have steady employment and want more money without a monthly fee, EarnIn is usually the better value; FloatMe’s edge is flexibility for people EarnIn won’t approve.

vs. Dave and Brigit: Both offer up to $500 — five times FloatMe’s max. Dave’s membership is only about $1 to $5 a month and its pricing recently simplified to a flat service fee, while Brigit runs a pricier $8.99 to $14.99 but bundles a credit-builder loan that reports to all three bureaus. Notably, Brigit holds a strong ~4.5 “Excellent” Trustpilot score against FloatMe’s ~2.2 — a gap worth weighing. FloatMe counters mainly on price (cheaper than Brigit) and simplicity, but on raw borrowing power and independent reputation, both rivals are ahead.

vs. free options like Klover, Current and Chime SpotMe: If your need is truly tiny, several apps do it without a subscription at all — Klover advances up to $200 free, Current’s Paycheck Advance goes up to $750 with no mandatory fee, and Chime’s SpotMe covers up to $200 in fee-free overdraft for Chime customers. FloatMe’s honest position in this crowded field is narrow: it makes sense mainly if you specifically want its budgeting tools and rent-reporting Premium tier, and if its low fee and flexible eligibility fit you better than the free alternatives.

Pros and Cons

What Users Love

A quick, no-interest bridge when it works: Satisfied members consistently say a small Float was exactly enough to cover gas, groceries or a bill and get them to payday without an overdraft. When you’re approved and the money lands, the interest-free, no-credit-check advance does the one job it promises, and owners appreciate not adding to their debt.

It helps some people stay in control: A recurring theme in positive reviews is that FloatMe’s small caps are a feature, not a bug — the app “doesn’t let me take out too much,” which some members value as a guardrail against over-borrowing. Paired with the balance alerts and forecasting, it can nudge better habits rather than deeper reliance.

Genuinely low cost for the category: At $4.99 a month, FloatMe is among the cheapest subscription options, and many members feel that’s fair for the bundle of an advance plus budgeting tools — especially compared with Brigit’s higher fee. For light users who tap the tools regularly, the price is easy to justify.

No credit impact, ever: Because FloatMe doesn’t report Float activity to the bureaus, a late or missed repayment won’t tank your credit the way a defaulted loan would — it simply pauses your eligibility for new Floats until you settle. For credit-cautious users, that safety is a real draw.

Strong app-store ratings and scale: With more than seven million downloads and lifetime app-store scores around 4.7 (iOS) and 4.4 (Android) across a very large number of reviews, a substantial base of members clearly find it useful day to day. That volume is a meaningful counterweight to the harsher independent reviews.

New credit-building and money tools: The Premium rent-reporting feature and the Subscription Manager are legitimately useful additions that most cash-advance apps lack — turning rent you already pay into credit history, and helping you claw back money lost to forgotten subscriptions.

Limitations Worth Knowing

You pay whether or not you’re approved: This is the number-one complaint, and it echoes the FTC’s core allegation. The $4.99 membership is charged upfront, but approval for a Float is never guaranteed — many members report paying the fee only to be told they don’t qualify, or to be capped at a token $20, with refunds hard to obtain. Confirm eligibility before you subscribe.

The lowest limits in the category: At a $100 maximum — and often far less in practice — FloatMe advances a fraction of what EarnIn, Dave, Brigit or MoneyLion offer. Long-time members frequently report their limit never rising above $20 despite spotless repayment, while rival apps raise limits over time. If you need real breathing room, this simply isn’t the tool.

A poor independent-review reputation: Here the signals genuinely conflict, and that conflict is the story. FloatMe’s app-store ratings sit near 4.7, but its Trustpilot score is roughly 2.2 out of 5 and its Better Business Bureau rating around 3.17 — with recurring complaints about denied advances, tiny limits, billing that continues after cancellation, and unresponsive support. When the marketplace ratings and the independent ratings diverge this sharply, both are telling you something, and the low independent scores deserve real weight.

Cancellation and billing friction: Even post-settlement, a real minority of reviewers report being charged after they believed they had cancelled, or discovering that deleting the app didn’t stop the debits. FloatMe now states clearly that uninstalling doesn’t cancel and that you must cancel in-app — but the burden is on you to follow the exact steps and keep the confirmation email.

Limited, portal-only support: FloatMe offers no customer-service phone number or email — the only channel is an online support portal (Zendesk), and responses can take a few business days. For a product people reach for in a financial pinch, slow and hard-to-reach support is a meaningful drawback that shows up repeatedly in negative reviews.

Overdraft risk and the FTC history: Because repayment is auto-debited on your payday, a mistimed pull against a low balance can trigger the very overdraft fee the app is meant to help you avoid — the alerts only help if you read them. And the 2024 FTC settlement over “free money” claims, hidden fees, dark-pattern cancellation and discrimination against public-assistance recipients is a serious mark on the company’s record that responsible buyers should factor in, even as they weigh the reforms that followed.

Beyond advances, FloatMe bundles forecasting, spending insights and low-balance alerts — the tools that, for many members, justify the $4.99 fee more than the small Floats do.

Who Should Use FloatMe

People who need a tiny, occasional bridge: If your gap is genuinely small — enough for gas or groceries, not a big bill — and you value an interest-free advance with no credit check, FloatMe is sized for exactly that. The key is to treat it as a rare buffer, not a monthly habit, and to lean on the free standard transfer when you can plan ahead.

Renters who want to build credit cheaply: FloatMe Premium’s rent reporting to TransUnion is a legitimate reason to consider the app, especially if you’re already paying rent on time and want it to count. For that specific goal, $12.99 a month can be reasonable value — provided you compare it against standalone rent-reporting services first.

Budget-minded users who’ll use the tools: If you’ll actually use the forecasting, spending insights and balance alerts to avoid overdraft fees, the low $4.99 membership can pay for itself even before you take a single Float. FloatMe is at its best as a budgeting bundle with a small advance attached, rather than the reverse.

Gig workers rejected elsewhere: Because FloatMe underwrites on your bank activity rather than strict employment verification, it can approve some freelancers and gig workers whom EarnIn’s W-2 requirements shut out. If more affordable, higher-limit apps have already turned you down, FloatMe’s flexibility is a genuine, if modest, alternative.

Who should look elsewhere: Anyone who needs more than $100, values a strong independent-review track record, or wants easy phone or email support should look past FloatMe. W-2 employees are usually better served by EarnIn’s fee-free, higher-limit model; people wanting credit building plus bigger advances should weigh Brigit; and anyone needing only a tiny free advance should check Klover, Current or Chime SpotMe first. Most importantly, if you’re relying on cash-advance apps every single pay period, that’s a signal to pause and build even a small buffer rather than pay recurring fees for shrinking amounts of your own next paycheck.

Getting Started: Step by Step

- Check eligibility first. Before anything else, confirm Floats are available in your state (they aren’t in Connecticut, DC or Nevada) and that your bank is supported. Doing this up front is the single best way to avoid paying a membership fee for a service you can’t actually use.

- Download the app and sign up. Create your account on your phone in a couple of minutes. Read the membership terms carefully — note that it’s $4.99/month, auto-renews, and that uninstalling later will not cancel it.

- Connect your bank account securely. Link your primary checking account through Plaid so FloatMe can review your income patterns, determine eligibility, deposit Floats, and later withdraw repayment. It won’t see your banking password.

- Get approved and check your limit. FloatMe reviews your account activity with no credit check. Expect a modest starting limit — often $10 to $20 for new members — and understand you build toward the $100 ceiling over time with consistent, on-time repayment.

- Request your Float and pick a speed. Choose an amount that fits your need, then select free standard delivery (1–3 business days) or pay the $1–$7 fee for an Instant Float. Repayment is automatically scheduled for your next payday, so make sure the funds will be there.

- Use the tools, or cancel cleanly. Lean on the forecasting and balance alerts to avoid overdrafts and get value beyond the advance. If FloatMe isn’t for you, cancel in-app (or via the online form), wait for the confirmation email, and only then delete the app.

FloatMe Premium ($12.99/month) reports your on-time rent to TransUnion, turning an expense you already pay into credit-building history — the app’s most compelling 2026 addition for renters.

Tips for Getting Maximum Value

Use the free standard transfer whenever you can plan even a couple of days ahead, and save the paid Instant Float for genuine same-day emergencies — on a small advance, the instant fee is a steep percentage of what you’re borrowing. Get real value from the membership by actually using the forecasting and low-balance alerts to head off overdraft fees, since those tools, not the tiny Floats, are where the $4.99 usually earns its keep. Only step up to Premium if you’ll use the rent reporting, and compare it against dedicated rent-reporting services before you commit. Borrow the smallest amount that solves the problem, set your repayment date with a clear eye on your balance so an auto-debit never triggers an overdraft, and avoid stacking advances across multiple apps. Keep your cancellation confirmation email in case a charge slips through, and — the honest bottom line — if you find yourself reaching for FloatMe every pay period, treat that as a prompt to build a small cash buffer instead, because paying recurring fees to access shrinking pieces of your own paycheck is the trap these apps can quietly become.

Future Outlook and Final Assessment

The cash-advance app market in 2026 is crowded and shifting. The “no mandatory fee” tier is shrinking as apps add or raise charges, credit-building features are becoming table stakes, and regulators are watching the whole category closely after enforcement actions against multiple players — FloatMe among them. In that environment, FloatMe has repositioned itself as a low-cost, tools-forward option and added a credit-building Premium tier, which is a sensible direction. The rent reporting in particular hints at where the value is heading: not the size of the advance, but the surrounding financial features.

The honest caveats are substantial and can’t be waved away. FloatMe advances the least money in its category, charges regardless of approval, carries a weak independent-review reputation next to a strong app-store one, and is working out from under a serious 2024 FTC settlement. Its reforms appear real — clearer fees, plainer cancellation language, a fair-lending program mandated by the order — but the burden is on the company to keep earning back trust, and on you to go in clear-eyed. Within a narrow lane — a genuinely small, occasional, interest-free bridge for someone who’ll use the budgeting tools — it can still do its job. Outside that lane, better-value options are easy to find.

Conclusion

FloatMe does one narrow thing and does it without interest or a credit check: it hands you a small amount of money to reach payday, then takes it back automatically. Around that core it has built genuinely useful budgeting tools and a new rent-reporting Premium tier that can build credit — real reasons it appeals to millions of members. But it also carries the lowest limits in its category, charges you whether or not you qualify, splits its reputation sharply between glowing app stores and harsh independent reviews, and is still rebuilding trust after a 2024 FTC settlement. That doesn’t make it a scam — it’s a licensed, regulated, and visibly reformed operator — but it does make it a product to approach with realistic expectations and a careful eye on the fees. Confirm your eligibility, use the free transfers and the tools, borrow only what you truly need, and cancel cleanly if it doesn’t fit. For a tiny bridge with budgeting on the side, FloatMe can help; for anything bigger, the alternatives are better — and World Of Tech’s job is to make that choice an easy one.

Need a small bridge to payday without the payday-loan pain?

Explore more honest reviews, tutorials and tech comparisons to find the right gear for the way you work, travel and live — at World Of Tech, where we make everything easy.

👉 Try FloatMe: https://floatme.com/

👉 Our YouTube Channel: youtube.com/@world_tech79

👉 Our Facebook Fanpage: Facebook

👉 Our X (Twitter): @worldoftech79

Pricing, features and policy details in this review were verified against floatme.com and independent sources (including the Federal Trade Commission, Trustpilot, the Better Business Bureau and hands-on reviewer testing) as of July 2026. Cash-advance app pricing, limits and policies change frequently, so confirm current details in the app before subscribing. Competitor prices are approximate and subject to change. This review is informational and not financial advice.

{kind=link}