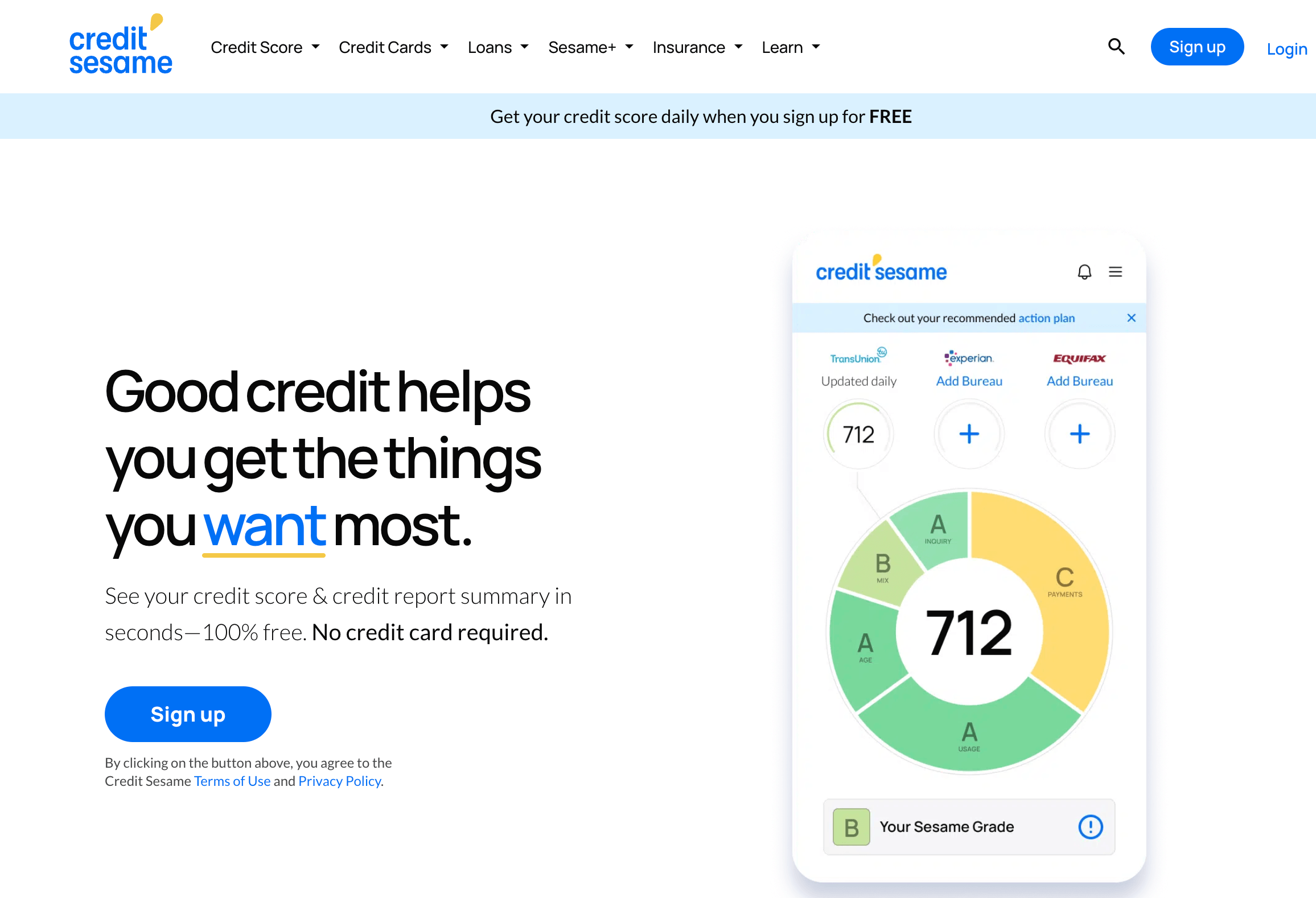

Your credit score quietly shapes more of your life than almost any other number: the mortgage rate you’re offered, whether you’re approved for a car loan, the apartment you can rent, the deposit a utility company asks for, and in many cases even a job offer. Yet most people have no real idea what’s moving that number up or down — and for years, simply seeing your own score meant paying the credit bureaus for the privilege. Credit Sesame was built to break that pattern. It’s a free credit and financial-wellness platform that gives you a daily TransUnion credit score, a plain-English letter grade explaining why your score is what it is, ongoing credit monitoring with alerts, and a personalized roadmap of actions to improve it — no credit card required and no impact on your score. Founded in 2010 by Adrian Nazari in the wake of the financial crisis, it has grown into one of the most established names in consumer credit, with more than 18 million members, an A+ Better Business Bureau accreditation, and a 2025 partnership that put its technology behind TransUnion’s own direct-to-consumer experience.

For anyone trying to build credit from scratch, recover from a rough patch, or simply keep an eye on their financial health, the appeal is obvious: genuinely useful tools that cost nothing to start. But Credit Sesame isn’t perfect, and an honest look turns up real trade-offs worth understanding before you sign up — a free tier limited to a single credit bureau, scores based on VantageScore rather than the FICO most lenders actually use, aggressive promotion of loan and credit-card offers, and a strikingly low public review rating that deserves context. This 2026 review walks through everything that matters: what Credit Sesame is and where it came from, the features that make it stand out, the full free-vs-paid pricing structure, head-to-head comparisons against Credit Karma and Experian, the genuine pros and cons drawn from real user feedback, and exactly who should — and shouldn’t — rely on it.

Credit Sesame Review 2026: The Free Credit Score App That Turns Your Number Into a Plan

Overview and Background

Credit Sesame is a US-based fintech company (Credit Sesame, Inc., headquartered in Mountain View, California) that offers free credit monitoring, credit-score education, identity-theft protection, and a full set of financial tools designed to help people understand and improve their credit. It isn’t a credit-repair agency that works on your behalf for a fee, and it isn’t a bank in the traditional sense — it’s a consumer platform built around one core idea its founder framed simply as “Assets minus Liabilities equals Wealth.” The premise is that plenty of services help you grow your assets, but few help you manage the liabilities side — your credit and loans — which is exactly where Credit Sesame positions itself as, in its own words, the financial advisor for your credit.

The company’s story is genuinely a milestone in personal finance. Founder and CEO Adrian Nazari, a Stanford Graduate School of Business alumnus, launched Credit Sesame after the 2008 financial crisis at a time when the major bureaus could charge consumers as much as $10 every time they wanted to look at their own credit data. After months of negotiating, he secured a contract with a credit bureau to provide free credit scores to consumers — one of the first times that had ever been done — helping spark the now-familiar era of free credit access. Fifteen years later, the company has raised roughly $161 million across multiple funding rounds from investors including Menlo Ventures, has been recognized as one of the most awarded credit apps in the industry (including “Best Personal Finance App” at the 2025 FinTech Breakthrough Awards), and serves a member base north of 18 million.

The most significant recent development is a 2025 collaboration with TransUnion. Credit Sesame’s underlying technology — branded “Sesame,” a turnkey, AI-powered credit-intelligence platform — now powers a new freemium direct-to-consumer credit education and monitoring experience for TransUnion, one of the three major US credit bureaus. Under the arrangement, Credit Sesame builds and runs the product platform, mobile app, and integrated network of financial offers, while TransUnion handles consumer acquisition, servicing, and compliance and migrates its existing US consumer base onto the new platform. In practical terms, that means the engine behind Credit Sesame is now trusted to operate at bureau scale — a strong signal of credibility, even as it also underscores how central data partnerships and financial-offer monetization are to how the business works.

Why Credit Sesame Stands Out in 2026

A genuinely free core, by deliberate design: Credit Sesame committed years ago to keeping its core credit monitoring perpetually free — no trial that flips to a charge, no credit card required to start. You can check your score, view a credit-report summary, and receive monitoring alerts indefinitely without paying a cent. For people who just want to keep an eye on their credit, that zero-cost baseline is the whole appeal.

Daily score updates, not monthly: Where most free services refresh your score once a month, Credit Sesame updates your TransUnion VantageScore 3.0 every day you log in. That cadence is genuinely useful — you can actually watch how your score responds after you pay down a balance, open a new account, or have a payment post, instead of waiting weeks to find out whether something worked.

The Sesame Grade explains the “why,” not just the number: A raw three-digit score tells you where you stand; it doesn’t tell you what to fix. Credit Sesame’s grading system assigns a clear letter grade built on the five major factors that drive your credit — payment history, credit usage, credit age, account mix, and inquiries — so you can see at a glance which area is dragging you down and where to focus your energy first.

An action plan, not just a monitor: This is the feature reviewers most often cite as Credit Sesame’s edge over simpler tools. Rather than only reporting your status, the platform analyzes your report and builds a personalized roadmap, prioritizing high-impact moves — like lowering utilization or correcting an error — and adapting its recommendations as your credit improves. It turns passive monitoring into an actual to-do list.

A “what-if” simulator for decisions before you make them: The score-simulator (sometimes called the credit-score potential tool) lets you model how a specific decision might move your score — paying off a card, taking out a new loan, or letting an account age — before you commit. For anyone planning a big financial step like a mortgage application, being able to test the impact in advance is a real advantage.

Built-in credit building through everyday spending: Through Sesame Cash, its no-fee digital banking account, Credit Sesame offers a Credit Builder feature that reports your everyday debit-card activity to the bureaus as positive payment history — a way to build credit without taking on a loan or a secured card. For people with thin or damaged files, that’s a meaningfully different on-ramp than most monitoring apps offer.

Pedigree, scale, and accreditation: Fifteen years in business, 18 million-plus members, nine patents, an A+ Better Business Bureau accreditation, and a platform trusted to power TransUnion’s own consumer experience all add up to a level of institutional credibility that newer credit apps simply can’t match. Whatever its imperfections, Credit Sesame is an established, serious player — not a fly-by-night marketplace product.

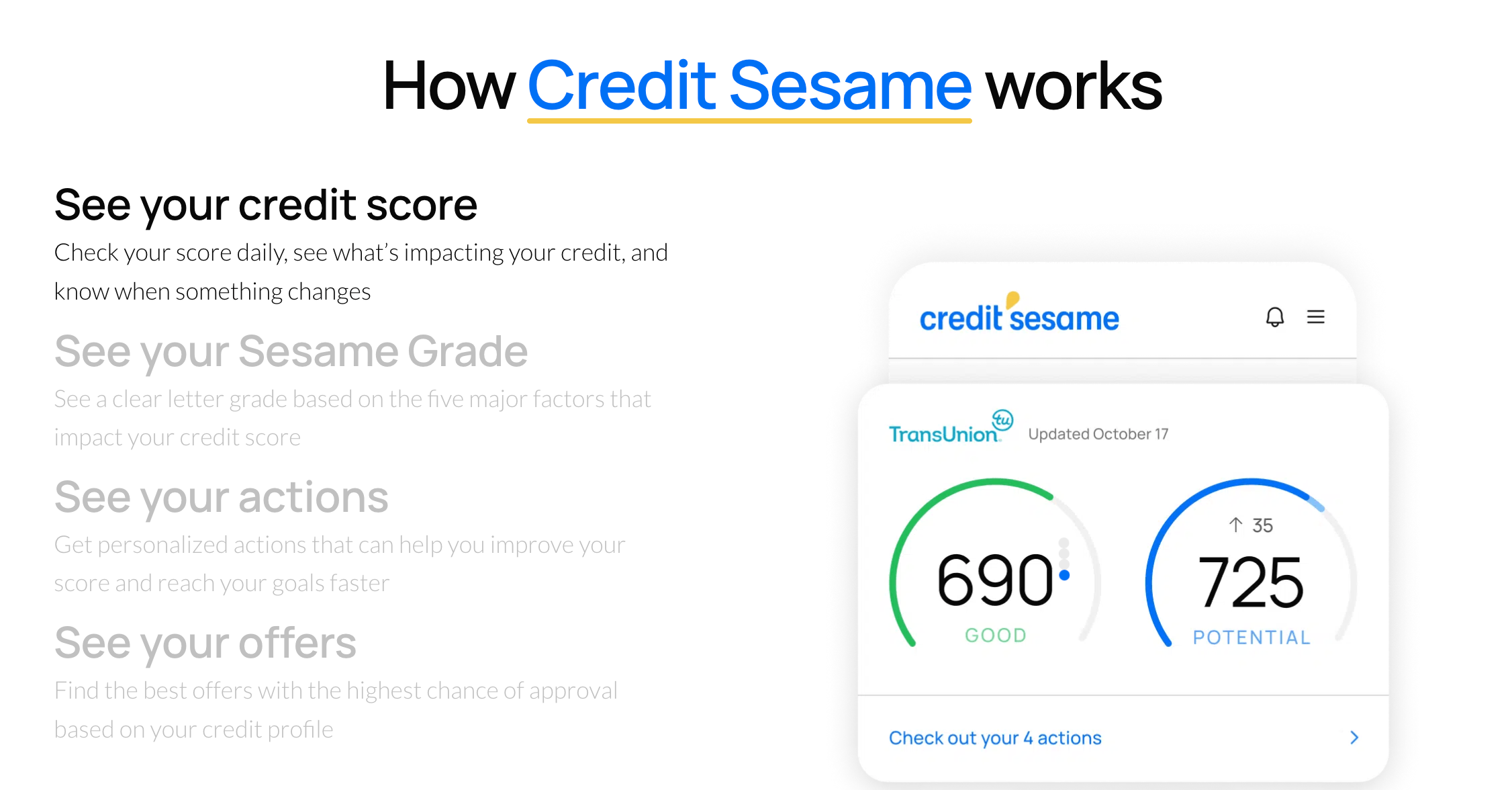

Credit Sesame refreshes your TransUnion score daily and pairs it with a letter-grade breakdown of the five factors driving it — so you see not just your number, but exactly what to work on next.

Key Features and Technology

Credit Sesame bundles a lot into one app, but its tools organize cleanly into a handful of pillars. Here’s how the platform actually breaks down.

Daily Credit Score and Sesame Grade

The foundation of the free experience is your TransUnion VantageScore 3.0, which uses the same familiar 300–850 range as FICO but is calculated with a different model. Credit Sesame refreshes it daily and layers the Sesame Grade on top — a letter grade derived from the five core credit factors (payment history, credit usage/utilization, credit age, account mix, and recent inquiries). One important honesty point: because VantageScore and FICO weigh things differently, and because most lenders pull FICO when you apply, your Credit Sesame number is best treated as a directional indicator of your credit health rather than the exact figure a bank will see.

Credit Monitoring and Alerts

Credit Sesame continuously watches your TransUnion credit report and pushes real-time alerts when something changes — a new account, a hard inquiry, a balance shift, or anything that could signal fraud or an error. You don’t have to log in and check manually; the platform notifies you when something worth knowing about happens. For people actively working on their credit or worried about identity theft, these alerts are one of the most practically valuable parts of the free tier, catching unauthorized account openings or unexpected dings early.

Score Simulator and Action Plan

Two tools work hand in hand here. The action plan reads your report and recommends prioritized steps to raise your score, re-ordering its advice as your situation evolves. The score simulator (or “what-if” tool) lets you estimate the impact of a specific move — paying down a card, opening or closing an account, adding a loan — before you actually do it. Together they shift Credit Sesame from a rear-view mirror into something closer to a planning tool, which is the main reason credit-builders tend to prefer it over a bare-bones score viewer.

Approval Odds and Personalized Offers

Credit Sesame matches you with credit-card, loan, and other financial offers based on your profile, and shows “Approval Odds” estimating your likelihood of being approved — useful for avoiding unnecessary hard inquiries on applications you’re unlikely to win. Its technology compares your profile against approved members and runs large numbers of scenarios to surface the offers most likely to fit. Be aware, though, that this recommendation engine is also how Credit Sesame makes money, and it’s the source of most complaints about being marketed to (more on that in the limitations section). Approval Odds are estimates, not guarantees of approval.

Sesame Cash and Credit Builder

Sesame Cash is Credit Sesame’s FDIC-insured digital banking account, with a Mastercard debit card and no minimum balance, monthly service, or foreign-transaction fees on the base account. Its standout is the Credit Builder feature, which reports your everyday debit purchases to the bureaus as on-time payments to help build positive history — and the platform can even reward score improvements with cash (members have been able to earn up to $100 in their first 30 days for improving their score). It’s a clever credit-building on-ramp, but read the fine print: some users report an inactivity fee and a monthly fee that applies unless it’s waived (it’s waived for Sesame+ subscribers or with qualifying activity), so it’s worth understanding the terms before you fund it.

Identity Protection and Three-Bureau Access

Stepping up to a paid Sesame+ plan unlocks the heavier protection: up to $1 million in identity-theft insurance, dark-web monitoring, fraud-resolution assistance, and access to your scores and full reports from all three major bureaus (Experian, Equifax, and TransUnion) rather than just one. Paid tiers also add rent reporting (to build history from on-time rent payments) and credit-dispute support to help challenge inaccuracies. These are the features that turn Credit Sesame from a free monitor into a more complete credit-and-identity package, and they’re the main reason to consider upgrading.

Pricing, Plans, and Package Structure

Credit Sesame runs on a freemium model: a genuinely free core, plus two optional paid tiers that add three-bureau coverage, identity protection, and credit-building extras. There’s no charge and no credit card required to use the free plan, and the paid plans come with a 7-day free trial. The figures below reflect Credit Sesame’s standard 2026 rates; pricing and plan features in fintech change frequently and you can often save by paying annually, so always confirm the live price and current plan details on the official site before subscribing.

| Plan | Price (USD) | What You Get | Best For |

|---|---|---|---|

| Free | $0 | Daily TransUnion VantageScore, Sesame Grade, credit-report summary, monitoring & alerts, score simulator, personalized offers | Anyone wanting to track & understand their credit at no cost |

| Sesame+ | $9.99/mo (7-day free trial) | Everything in Free plus three-bureau scores, identity alerts, fraud resolution, $1M ID-theft insurance, credit-building tools | Active credit-builders wanting full-bureau view & protection |

| Sesame+ Complete | $19.99/mo (7-day free trial) | All Sesame+ features plus the most comprehensive monitoring, dispute support, and rent reporting | Power users wanting maximum coverage & identity defense |

| Sesame Cash + Credit Builder | $0 base (fee waived with Sesame+ or qualifying activity) | FDIC-insured debit account that reports debit spending as on-time payments; cash rewards for score gains | Thin or damaged files building credit via everyday spending |

How Credit Sesame Compares to Alternatives

| Factor | Credit Sesame | Credit Karma | Experian |

|---|---|---|---|

| Free tier cost | Free | Free | Free (paid plans extra) |

| Bureaus (free tier) | 1 (TransUnion) | 2 (TransUnion + Equifax) | 1 (Experian) |

| Score model | VantageScore 3.0 | VantageScore 3.0 | FICO + VantageScore |

| Update frequency | Daily | Weekly | Varies (often daily on app) |

| Credit-building tools | Sesame Cash, Credit Builder, rent reporting | Credit Builder (via savings) | Experian Boost, rent reporting |

| Identity-theft insurance | Up to $1M (paid plans) | Not a core focus | Up to $1M (paid plans) |

| Best for | Daily tracking + an action plan to improve | Two-bureau free view + full reports | Seeing a real FICO score for free |

vs. Credit Karma: Credit Karma is Credit Sesame’s most direct free rival and arguably the more generous monitor — its free tier covers two bureaus (TransUnion and Equifax) with full reports, versus Credit Sesame’s single bureau. Where Credit Sesame pulls ahead is daily (rather than weekly) score updates, the Sesame Grade, and a more structured action plan aimed squarely at improving your score rather than just displaying it. If you want the widest free data picture, Credit Karma wins; if you want a coaching-style tool with daily feedback, Credit Sesame is the stronger fit. Many people simply use both.

vs. Experian: Experian’s biggest advantage is that, as one of the three bureaus, its free app can show you an actual FICO score — the model most lenders use — alongside Experian Boost, which adds utility and streaming payments to your file. Credit Sesame counters with daily VantageScore updates, a clearer improvement roadmap, and a broader credit-building toolkit through Sesame Cash. If matching exactly what a lender will see matters most to you, lean Experian; if you want an action-oriented dashboard, Credit Sesame holds up well.

vs. paid identity-protection services: Dedicated identity suites like LifeLock or IdentityForce go deeper on monitoring and restoration, but they charge monthly from the first day. Credit Sesame’s paid Sesame+ tiers bundle up to $1 million in identity-theft insurance and dark-web monitoring at a competitive price, layered on top of credit tools you may already be using — making it a reasonable all-in-one for people who want credit and identity protection in a single app rather than a standalone security product.

Against free rivals, Credit Sesame trades broader bureau coverage for daily updates and a stronger improvement plan — which is why many people run it alongside Credit Karma or Experian rather than instead of them.

Pros and Cons

What Users Love

Free, frictionless access to your credit: The most consistent praise is the simplest: a genuinely free credit score and report summary with no credit card required, delivered in seconds. Many users describe finding Credit Sesame, checking their score in minutes, and getting clear, actionable information at zero cost — a low-stakes way to start paying attention to their credit.

It actually helps people improve: Long-time members frequently report real results — rebuilding from “poor” to “good” or “excellent” over a year or so by following the platform’s guidance, or using its insights to qualify for a first credit card, refinance a high-rate car loan, or finally buy a home. The combination of daily feedback and a prioritized plan is what they credit for the progress.

Daily updates and a plain-English grade: Reviewers value seeing their score move day to day and appreciate the letter grade for translating an abstract number into something they can act on. It removes a lot of the mystery that makes credit feel intimidating, especially for first-timers.

Useful monitoring and fraud alerts: The real-time alerts for new accounts, inquiries, and changes are a recurring favorite, giving people confidence that they’ll catch suspicious activity early without having to remember to log in and check.

An established, accredited name: Users take comfort in Credit Sesame’s longevity, its A+ BBB accreditation, bank-level encryption, and the fact that checking your own score is a soft inquiry that won’t hurt it. For a free service, that institutional backing matters.

Helpful personalized offers — when relevant: When the recommendation engine is well-matched, members appreciate being pointed to a credit card or refinance they qualified for and got approved for, sometimes with no annual fee or with cash back — turning the platform’s monetization into a genuine win for the user.

Limitations Worth Knowing

A strikingly low public review rating: This needs to be said plainly: Credit Sesame’s Trustpilot rating sits around 1.1 out of 5 across roughly 2,100 reviews. That’s very low, and it deserves honest context — free credit and fintech services skew heavily toward complaint-driven reviews, many of the harshest reviews target Sesame Cash or loan-offer spam rather than the core monitoring, and the same platform holds an A+ BBB accreditation and 18 million-plus members. Still, the volume of frustration is real, and you should go in clear-eyed rather than assume a flawless experience.

Aggressive offers and lead-related spam: The single most common complaint is being marketed to relentlessly. Because Credit Sesame earns revenue by referring you to financial products, some users report a steady stream of credit-card and loan offers — and, in the worst cases, ongoing calls or emails they attribute to their information being used for lead generation. If you value a quiet inbox, this is the trade-off for a free service.

One bureau and VantageScore, not FICO: The free tier shows only your TransUnion data, while rivals like Credit Karma show two bureaus for free. And the VantageScore 3.0 it reports isn’t the FICO score most lenders pull, so the number you see may differ — sometimes meaningfully — from what a bank uses to make a decision. It’s a directional guide, not a guaranteed match.

Sesame Cash issues for some users: While the Credit Builder concept is appealing, a portion of reviews describe real problems with Sesame Cash — confusion over fees (an inactivity fee and a monthly fee that applies unless waived), account-access and security scares, and difficulty getting help when something went wrong. Read the terms carefully and weigh whether you need the banking product at all before funding it.

Best features sit behind the paywall: Three-bureau scores, identity-theft insurance, dispute support, and rent reporting all require a paid Sesame+ plan. Compared with what some free services offer, parts of the free experience can feel thin, and getting the full value generally means subscribing.

US-only, and not a replacement for the full picture: Credit Sesame is built around the US credit system and its bureaus, so it isn’t usable for credit outside the US. And because the free tier is single-bureau, getting a complete view still means supplementing it — for example with the federally mandated free annual reports from AnnualCreditReport.com — rather than relying on Credit Sesame alone.

Who Should Use Credit Sesame

Credit-builders and people recovering from a rough patch: This is Credit Sesame’s sweet spot. If your goal is to raise your score — not just watch it — the daily updates, Sesame Grade, action plan, and credit-building tools give you a clear, feedback-rich path forward. Users rebuilding from poor credit feature heavily and positively in the reviews.

First-timers learning how credit works: If credit has always felt like a black box, the plain-English grade and educational framing make Credit Sesame an approachable starting point. It’s a low-pressure way to understand what’s helping and hurting your score before you make a big financial move.

People with thin files who want to build without debt: The Sesame Cash Credit Builder — reporting everyday debit spending as on-time payments — is a genuinely useful on-ramp for anyone with little or no credit history who’d rather not open a loan or secured card to get started.

Anyone wanting free monitoring and an identity safety net: For free, ongoing alerts and the option to add up to $1 million in identity-theft insurance through a paid tier, Credit Sesame is a sensible all-in-one for people who want credit tracking and identity protection in a single app rather than juggling separate tools.

Who should look elsewhere: If you specifically need the FICO score lenders use, Experian’s free FICO or a service that surfaces FICO is a better match. If you want the broadest free data, Credit Karma’s two-bureau coverage edges it out. People outside the US can’t use it at all, and anyone who can’t tolerate marketing offers — or who only wants a bare score with zero upsell — may find the steady stream of recommendations and the paywalled premium features frustrating. As always, supplement any single tool with your free annual bureau reports for the complete picture.

Credit Sesame is at its best for people actively building or rebuilding credit — the daily score, action plan and Credit Builder tools turn monitoring into measurable progress.

Getting Started: Step by Step

- Sign up for the free plan. Create an account on the website or mobile app with no credit card required. Verifying your identity triggers only a soft inquiry, so signing up will not hurt your credit score. Within seconds you’ll see your TransUnion score, your Sesame Grade, and a summary of your report.

- Read your grade before your number. Don’t fixate on the three digits — open the Sesame Grade and see which of the five factors (payment history, usage, age, mix, inquiries) is weakest. That’s where the fastest gains usually are, and it tells you what to prioritize.

- Turn on monitoring and alerts. Make sure notifications are enabled so you’re told about new accounts, hard inquiries, and balance changes in real time. This is your early-warning system for both errors and fraud, and it’s free.

- Build a plan with the simulator. Use the action plan and “what-if” simulator to model moves before you make them — for example, see how paying a card down to under 30% utilization, or holding off on a new application, is estimated to affect your score. Then act on the highest-impact step first.

- Consider credit-building tools if your file is thin. If you have little history, look at Sesame Cash and the Credit Builder feature to report everyday spending as on-time payments — but read the fee terms first and only fund it if it fits your situation.

- Upgrade only if you have a specific need. Stay on the free plan unless you genuinely want three-bureau visibility, identity-theft insurance, dispute support, or rent reporting. If so, use the 7-day Sesame+ trial to test it, and set a reminder to cancel before it converts if it isn’t worth it.

Tips for Getting Maximum Value

Treat Credit Sesame as a coaching dashboard rather than a scoreboard: the daily number only helps if you act on the grade and alerts, so make lowering your credit utilization, paying every bill on time, and disputing any genuine errors your standing priorities. Remember that the VantageScore you see is directional — pair it with a look at your actual FICO (through your bank or a FICO-based service) before any major application like a mortgage, and pull your free reports from all three bureaus at AnnualCreditReport.com to catch anything Credit Sesame’s single-bureau free view might miss. Be disciplined about the offers: the recommendation engine is marketing, so only apply for cards or loans you’d have sought out anyway, and lean on the Approval Odds to avoid wasted hard inquiries. If you try Sesame Cash, read the fee terms first and keep the account active (or pair it with Sesame+) to avoid charges. And if the promotional emails and offers become too much, tighten your notification and communication settings rather than abandoning a tool that’s otherwise doing its job for free.

Future Outlook and Final Assessment

The free-credit space in 2026 is crowded and maturing, but Credit Sesame has aged into one of its more credible operators. Fifteen years in, with 18 million-plus members, nine patents, industry awards, and a 2025 collaboration that put its technology behind TransUnion’s own consumer experience, it has clearly moved beyond the “is this legit?” question. The direction of travel — AI-driven credit intelligence, deeper personalization, and tighter integration with a major bureau — suggests the underlying platform will only get more capable, and the core promise of free daily scores plus an actionable plan to improve them remains genuinely useful.

The honest caveats are equally real and unlikely to vanish: a free tier limited to a single bureau and a non-FICO score, a business model built on financial-offer referrals that generates marketing fatigue and lead-related complaints, mixed experiences with Sesame Cash, and a public review rating that — context aside — is hard to ignore. The smartest way to read all of that is as a profile, not a verdict: Credit Sesame is excellent at what it’s actually for (free, daily, improvement-focused credit tracking) and weaker where it tries to monetize or where you need the full lender’s-eye picture. Used for its strengths and supplemented for its gaps, it earns its place.

Conclusion

Credit Sesame set out to make credit free, understandable, and improvable — and on that core mission it largely delivers. By giving you a daily score, a letter grade that explains it, real-time monitoring, and a personalized roadmap at no cost, it removes the two biggest barriers most people face with their credit: not knowing the number, and not knowing what to do about it. It rewards realistic expectations and active use, and it isn’t the right pick for FICO purists, marketing-averse users, or anyone outside the US — but for the everyday reality of building, monitoring, and protecting your credit, few free tools offer more. Sign up for the free plan, act on what it shows you, keep your other free reports handy, and Credit Sesame can take a lot of the mystery out of your financial health and make it genuinely easier to manage.

Ready to see your credit score and turn it into a plan?

Explore more honest reviews, tutorials and tech comparisons to find the right tools for the way you work, save and live — at World Of Tech, where we make everything easy.

👉 Try Credit Sesame: https://www.credit-sesame.com

👉 Our YouTube Channel: youtube.com/@world_tech79

👉 Our Facebook Fanpage: Facebook

👉 Our X (Twitter): @worldoftech79

Pricing, plan details and features in this review were verified against creditsesame.com and independent review sources (including Trustpilot, the Better Business Bureau, and hands-on reviewer testing) as of June 2026. Credit Sesame is a US-focused service, and credit-monitoring pricing, plans and features change frequently, so confirm current details on the official site before subscribing. Competitor details and prices are approximate and subject to change.

{kind=link}